Confused about choosing between a Consolidation Loan and Debt Review? Let DCGsa help you find the best solution for your financial situation.

Deciding between debt review and a consolidation loan depends on your financial situation, habits and goals. Both options aim to make debt more manageable, but they work differently and serve different purposes. Let’s explore their key differences.

What Is Debt Review?

Debt review restructures your debt repayments through a legal process. A debt counsellor assesses your financial situation, negotiates with creditors, and creates a repayment plan that proposes reduced monthly installments and interest rates. The National Credit Act (NCA) regulates debt review, which legally protects over-indebted consumers.

What Is a Consolidation Loan?

Debt relief options – To consolidate multiple loans, you add up what you owe on all your debts and apply for a new loan to settle them all. This approach simplifies payments by consolidating your debt under one lender however there is still high interest rates, initiation fee, service fees etc. that need to be paid on this loan. Qualifying for a consolidation loan requires a good credit score and proof of affordability. And If you are not diligent to use the funds to pay off your other debt, you put yourself in a worse situation.

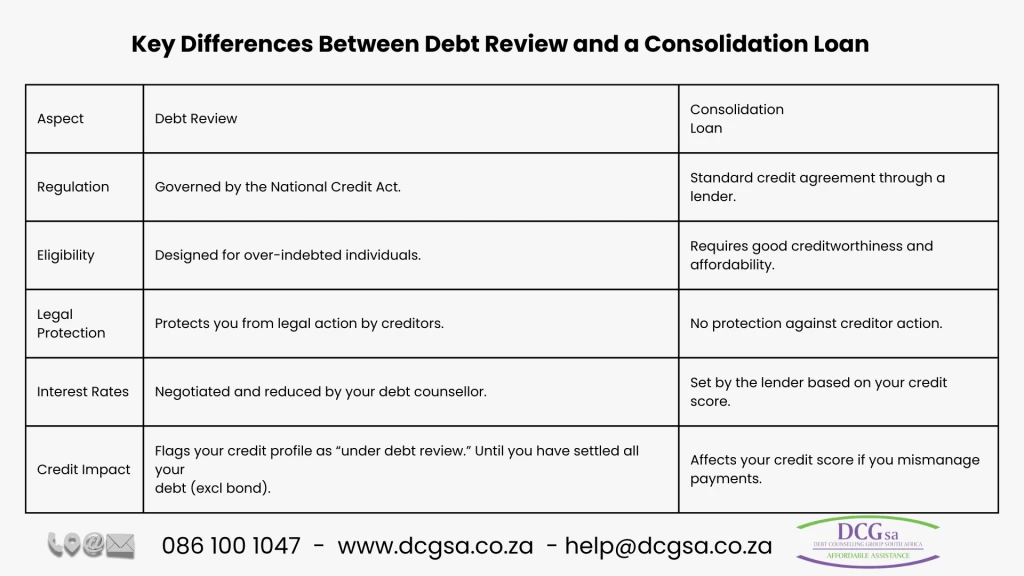

Key Differences Between Debt Review and a Consolidation Loan

[rev_slider alias="Home_Page" slidertitle="Home Page"][/rev_slider] Confused about Debt Review vs. Consolidation Loans? This quick comparison chart shows the key differences to help you make an informed decision.

When Should You Choose Debt Review?

- Your debt exceeds your ability to repay it.

- Or you Pay your debts and have nothing left for your household needs.

- You need protection from creditors and legal action such as vehicle or home repossession.

- Your credit score is too low and you are rejected for credit due to too much negative profile history.

- You prefer a structured, solution to pay off debt with a professional to guide you.

When Should You Choose a Consolidation Loan?

- Your credit score qualifies you for favorable loan terms.

- You want to simplify multiple debts into one payment.

- You have manageable debt and don’t need additional help.

- You feel confident in managing your finances independently.

Which Option Is Right for You?

Debt review works best for over-indebted individuals who need legal and financial relief. A consolidation loan suits consumers with good credit who want to streamline their debt into one manageable payment.

Contact DCGsa for Expert Guidance

Not sure which option fits your needs? DCGsa provides professional advice to help you make an informed choice about your financial future.

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For more details, visit our Debt Counselling Services page.

")