October is Mental Health Awareness Month: How Debt Impacts Your Mind

October is Mental Health Awareness Month in South Africa. Did you know that debt and mental health are deeply connected? Across the country, thousands of people struggle with financial stress and anxiety, which often leads to burnout, depression, and strained relationships. At DCGsa — South Africa’s trusted debt review specialists — we believe financial freedom equals mental freedom. Taking control of debt stress is not only about money, it is also about protecting your peace of mind, your relationships, and your future.

At DCGsa (Debt Counselling Group South Africa), we believe:

👉 Financial freedom = mental freedom.

When your money is under control, so is your peace of mind.

The Hidden Link Between Debt and Mental Health

Debt affects more than just your bank account. In fact, financial stress is one of the leading triggers of mental health challenges in South Africa. Counselling Psychologist Christelle Van Tonder explains in Smart Wealth Magazine:

“Debt can cause significant emotional and psychological stress, which can manifest in anxiety, depression, suicidal ideation, sleep disturbances, physical symptoms, strained relationships, and feelings of shame and guilt.”

How Debt Strains Relationships

Counselling Psychologist Christelle Van Tonder explains in Smart Wealth Magazine:

“Debt can cause significant emotional and psychological stress, which can manifest in anxiety, depression, suicidal ideation, sleep disturbances, physical symptoms, strained relationships, and feelings of shame and guilt.”

When you’re living under the pressure of unpaid bills, creditor calls, or fear of repossession, it doesn’t just stay on paper. It impacts your body, your sleep, your relationships — and your hope for the future.

How Debt Strains Relationships

Money is one of the leading causes of relationship conflict in South Africa. Christelle highlights:

“Couples struggling with debt often avoid discussing financial issues, budgeting together and being transparent about spending habits. This can lead to conflict, trust difficulties and resentment — which ultimately stifles intimacy and emotional connection.”

At DCGsa, we’ve seen how addressing debt together can restore not only financial stability, but also healthier, stronger relationships.

Taking the First Step: From Shame to Strength

Many South Africans feel embarrassed about asking for help with debt. But as Christelle says:

“Debt review is not a sign of failure, but a step towards financial freedom. You’ve taken the first step by acknowledging your situation and seeking help. Stay committed, be patient, and celebrate your progress. You got this!”

Talking about money stress isn’t weakness — it’s courage.

Practical Tips for Protecting Your Mental & Financial Health

DCGsa: Standing With You This Mental Health Awareness Month

This October, we stand with every South African fighting silent battles.

At DCGsa, our mission is to lighten the load by giving you the tools, guidance, and protection to rebuild your financial and emotional well-being.

Want deeper insights from Christelle Van Tonder on mental health and debt?

She shares her expertise in a 2-page feature article in the latest issue of Smart Wealth Magazine.

Frequently Asked Questions about Debt Counselling

Can I Leave Debt Review?

Many people ask us: “What if I change my mind — can I leave debt review?” At DCGsa, we explain it like this: debt review is designed to protect you, not trap you. Once you step in, it works like a lifeboat when you’re caught in a storm.

Why You Can’t Just Get Out of Debt Review

Imagine you’re in a small boat that’s taking on water. You have two choices:

Which choice will get you to shore safely? Debt review is like plugging the holes — it protects your home, car, and family from sinking under debt.

Exiting Debt Review Before a Court Order

If you’ve only just started and your case hasn’t gone to court yet, the court can still look at your situation. If they find you are not actually over-indebted, then debt review will end there. But this is a court decision, not something you can just choose on your own.

Exiting Debt Review After a Court Order

Once the court has approved your repayment plan, you’re fully protected. From here, you can’t just walk away — but that’s a good thing. It means creditors can’t take your car or home while you’re under the plan.

The only safe way out is to finish the plan or pay off the debts early. When you do, you’ll get a clearance certificate that wipes the debt review flag from your name.

Beware of False Promises Regarding Exiting Debt Review

Some companies claim they can “remove you from debt review” for a big fee. The NCR warns these services are fake and often take money without helping at all. DCGsa never charges such fees. The only real way out is by following the law and completing your plan safely.

Key Takeaways

You cannot simply leave debt review, but that’s because it’s built to protect you until you’re safe again. Think of it like staying in the lifeboat — it may take time, but it’s the safest way to reach financial freedom. At DCGsa, with Casper le Grange, you are never alone on this journey.

Latest National Credit Regulator Update on Exiting Debt review

What is Debt Review?

Debt review is a legal process in South Africa, established under the National Credit Act (NCA), and it is specifically designed to assist consumers who are struggling to repay their debts. Through this process, you gain breathing space from relentless creditor pressure, while at the same time ensuring that your assets are protected. At DCGsa, our goal is not only to guide you through each step but also to help you steadily work towards a debt-free future — all under the expert care of our NCR-registered Debt Counsellor, Casper le Grange.

Debt Review Gives You Legal Protection Against Creditors

Once you enter debt review, your creditors cannot take legal action against you for unpaid debts (as long as you make your agreed repayment). All credit provider communication must go through us. This means no more threatening calls or letters, giving you peace of mind from the very beginning.

How Debt Review Works

The process begins when you apply with DCGsa. We:

You pay a single reduced instalment every month through a Payment Distribution Agency (PDA). From there, the funds are securely distributed to all your creditors, and at the same time, you receive a monthly Distribution Statement. This way, you can clearly see how much each credit provider has been paid.

What Debts Are Included under Debt Review?

Debt review covers most credit agreements, including:

It does not cover monthly living expenses (groceries, school fees, insurance, etc.), but by reducing your debt repayments, debt review frees up more money for these essentials that we assist you in budgeting for so you are not left wondering how to get through a month.

Debt Review End Goal: Debt Freedom

Debt review is not permanent. Once your repayment plan is complete, you’ll receive a clearance certificate that confirms all your debts have been paid off (or paid as agreed). At this point, the debt review flag is removed from your credit profile, and you’re free to take on credit again — this time with a clean slate.

Casper le Grange explains it clearly:

“Debt review is not about restricting you; instead, it’s about protecting you. In addition, it helps you rebuild your finances, and ultimately, it gives you back full control of your life.”

Debt review is a legal and structured process that not only protects you from creditors but also reduces your monthly repayments. As a result, it helps you pay off debt in a safe and at the same time affordable way. With DCGsa — and more importantly, with the personal guidance of Casper le Grange — you gain both the expertise and the support you need to finally become debt free.

Error: Contact form not found.

You may also enjoy this -

How Debt Review Actually Works (in Plain English)

How immediate is Debt Relief through Debt Review?

At DCGsa, one of the most common questions we get is: “How quickly will I feel the relief once I enter debt review?” The good news is that the relief begins almost immediately, both emotionally and financially.

Immediate Emotional Relief (Day One)

The moment you apply for debt review with DCGsa, your creditors can no longer harass you with calls, emails, or threats of legal action. We immediately send a formal notification to all your credit providers — which means they must deal directly with us, not you.

This step alone gives most clients a powerful sense of relief and control from day one.

First Financial Relief (First Month)

Once we’ve reviewed your budget and restructured your debts, you’ll make your first reduced repayment through an accredited Payment Distribution Agency (PDA).

For most clients, this new single payment is significantly lower than what they were paying before. That means more money left in your household budget for essentials like groceries, school fees, and transport.

Long-Term Debt Freedom (Commitment & Consistency)

Debt review is not a “quick fix” — it’s a structured, legal process under the National Credit Act (NCA). While emotional relief is immediate, and financial relief begins with your first reduced payment, true debt freedom takes commitment.

As Casper le Grange, our NCR-registered Debt Counsellor with over 15 years of experience, reminds clients:

👉 “Your debt doesn’t disappear overnight, but the first step in debt review gives you breathing space again — and that breathing space is life-changing.”

✅ Key Takeaway

Debt relief with DCGsa is immediate in terms of protection from creditors and emotional peace of mind. Financial relief begins with your first reduced repayment, and long-term debt freedom is achieved by sticking to the plan.

Pay One Affordable Monthly Payment towards ALL Your Debt. No Juggling Payments anymore.

We negotiate for Reduced Debt Repayments. So you pay your reduced payment from your next pay date, giving relief from your next pay date.

Your assets are protected by law. Creditors must stop legal action, including repossession or garnishee orders, as long as you comply with the agreed plan.

Debt Review isn’t just about managing payments—it’s about reclaiming your life.

You will get immediate stress relief once you apply for our services.

Error: Contact form not found.

How Long Does Debt Review Last?

Many South Africans ask, “How long does debt review last?” The answer depends on your unique financial situation. Debt review is designed to give you a structured repayment plan so you can become debt free in a realistic timeframe. On average, most consumers complete the process in 3 to 5 years, but the duration varies depending on debt size, repayment consistency, and interest rates.

Understanding How Long Does Debt Review Last in South Africa?

Debt review does not have a fixed end date for everyone. Your repayment plan is calculated according to your monthly affordability and the agreements made with your credit providers. Some consumers complete the process in as little as two years, while others may take longer than five years if their debt load is higher.

Factors That Affect the Debt Review Timeline

Several factors influence how long debt review lasts for you:

Court Approval of Debt Review Repayment Plan and Term

Once DCGsa has negotiated reduced interest rates, lower monthly repayments, and adjusted fees, the next step is going to court. The court order makes your new repayment plan legally binding, ensuring that credit providers must stick to the agreement. At this stage, you’ll also see the exact term for each debt if you stick to your repayment plan. This gives you a clear timeline and peace of mind about when you’ll finally be debt free.

When Debt Review Ends: The Clearance Certificate

Debt review officially ends when all your debts included in the process are fully repaid. At that point, your debt counsellor issues a clearance certificate. This certificate is then sent to the credit bureaus, and they update your profile to reflect that you are debt free.

How DCGsa Helps You Complete Debt Review Successfully

At DCGsa, we guide you through every step of the journey. Our team ensures your repayment plan is manageable, helps you stay on track with payments, and communicates with credit providers on your behalf. With our support, you can complete the process faster and enjoy the freedom of a fresh financial start.

Contact DCGsa for Expert Guidance – Or find out if you qualify for debt review.

If you’re considering debt review and need professional advice, DCGsa is here to assist you every step of the way.

- Call us: 086 100 1047

- Email us: help@dcgsa.co.za

- WhatsApp us: 061 432 8499

- Watch our videos on YouTube: DCGsa Debt Counselling Group

For more information, on How Debt Counselling Works – CLICK HERE

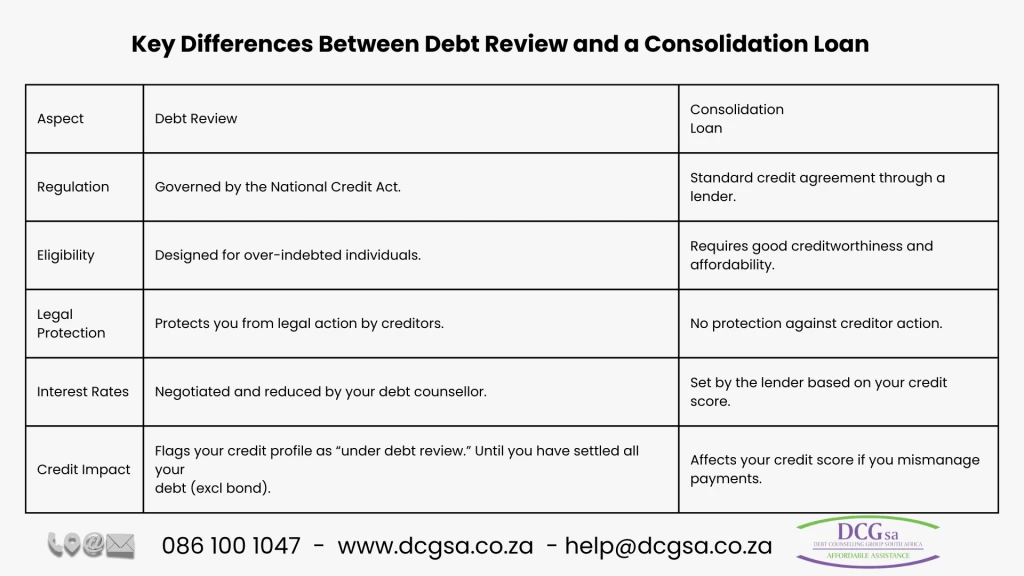

Confused about choosing between a Consolidation Loan and Debt Review? Let DCGsa help you find the best solution for your financial situation.

Deciding between debt review and a consolidation loan depends on your financial situation, habits and goals. Both options aim to make debt more manageable, but they work differently and serve different purposes. Let’s explore their key differences.

What Is Debt Review?

Debt review restructures your debt repayments through a legal process. A debt counsellor assesses your financial situation, negotiates with creditors, and creates a repayment plan that proposes reduced monthly installments and interest rates. The National Credit Act (NCA) regulates debt review, which legally protects over-indebted consumers.

What Is a Consolidation Loan?

Debt relief options – To consolidate multiple loans, you add up what you owe on all your debts and apply for a new loan to settle them all. This approach simplifies payments by consolidating your debt under one lender however there is still high interest rates, initiation fee, service fees etc. that need to be paid on this loan. Qualifying for a consolidation loan requires a good credit score and proof of affordability. And If you are not diligent to use the funds to pay off your other debt, you put yourself in a worse situation.

Key Differences Between Debt Review and a Consolidation Loan

[rev_slider alias="Home_Page" slidertitle="Home Page"][/rev_slider] Confused about Debt Review vs. Consolidation Loans? This quick comparison chart shows the key differences to help you make an informed decision.

When Should You Choose Debt Review?

- Your debt exceeds your ability to repay it.

- Or you Pay your debts and have nothing left for your household needs.

- You need protection from creditors and legal action such as vehicle or home repossession.

- Your credit score is too low and you are rejected for credit due to too much negative profile history.

- You prefer a structured, solution to pay off debt with a professional to guide you.

When Should You Choose a Consolidation Loan?

- Your credit score qualifies you for favorable loan terms.

- You want to simplify multiple debts into one payment.

- You have manageable debt and don’t need additional help.

- You feel confident in managing your finances independently.

Which Option Is Right for You?

Debt review works best for over-indebted individuals who need legal and financial relief. A consolidation loan suits consumers with good credit who want to streamline their debt into one manageable payment.

Contact DCGsa for Expert Guidance

Not sure which option fits your needs? DCGsa provides professional advice to help you make an informed choice about your financial future.

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For more details, visit our Debt Counselling Services page.

Can debt review be removed? Understand the legal provisions, including repayment or court orders, required to exit debt review. Contact DCGsa for expert guidance today.

Can Debt Review Be Removed?

No, a consumer cannot voluntarily remove themselves from debt review once the process has been initiated according to the National Credit Act (NCA). Debt review is a legal process designed to assist over-indebted individuals, and its removal is governed by strict legal provisions.

When Can a Consumer Exit Debt Review?

After Full Repayment:

- Once all debts, excluding a home loan, are fully repaid, the debt counsellor may issue a clearance certificate in terms of Section 71 of the NCA. This is the only way to exit debt review after a court order has been granted. Receiving a clearance certificate is like pressing reset on your credit report. It removes any record that you were ever under debt review and removes all adverse credit report information, leaving you with a fresh start.

Before a Magistrate Court Order:

- If the consumer has been determined to be over-indebted but no court order has been granted, they may present new facts to the Magistrate Court. If the court finds the consumer not over-indebted, the debt review process ends, and the credit bureaus are updated accordingly. This will however affect your credit record as it will only remove the debt review flag and not any adverse information such as – missed payments, short payments or any other negative information regarding your credit profile.

When Can’t Debt Review Be Removed?

Voluntary Withdrawal:

- Once a consumer applies for debt review in the prescribed manner (Form 16), they cannot voluntarily withdraw from the process. The Van Vuuren judgment clarified that the NCA does not allow for voluntary withdrawal after application.

After a Magistrate Court Order:

- If a debt re-arrangement order has been granted by the court, the consumer must complete the repayment plan or obtain a clearance certificate to exit debt review.

High Court Orders:

- The Magistrates Court nor The High Court can terminate a debt review process or declare a consumer no longer over-indebted.

What Happens If a Consumer’s Financial Situation Improves?

When a consumer’s financial situation improves during debt review, they should increase their debt review payments or settle debts to shorten the repayment term. Taking these proactive steps helps them exit debt review sooner through a Form 19 Clearance Certificate, achieving financial freedom faster than initially planned.

Contact DCGsa for Expert Guidance

If you’re under debt review and unsure of your options, DCGsa can guide you with professional advice and support tailored to your needs.

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

Free Credit Check and Debt Assessment – Click Here.

Learn more on this News24 Article that our Debt Counsellor Casper le Grange was quoted in.

Learn how to exit debt review legally and effectively with Form 19. Expert advice from Casper le Grange, featured on News24.

Consumers gain a structured and legally protected pathway to manage and overcome over-indebtedness by engaging with a registered debt counsellor like Casper le Grange (NCRDC1560). The National Credit Act establishes a regulatory framework, and the National Credit Regulator enforces it to ensure debt counsellors maintain high standards of professionalism. This approach gives consumers peace of mind and a practical solution for achieving financial stability.

No, debt review is not the same as administration. While both are legal debt solutions for consumers, they are distinct processes governed by different laws and suited for different financial situations. Debt review falls under the National Credit Act (NCA), while administration is regulated by the Magistrates’ Court Act.

5 Differences Between Debt Review and Administration

- Governing Legislation:

- Debt Review: Regulated by the National Credit Act (NCA).

- Administration: Governed by the Magistrates’ Court Act.

- Debt Limitations:

- Debt Review: No limit to the amount of debt; suitable for individuals with larger debt loads.

- Administration: Only applies to debts below R50,000.

- Assets Protection:

- Debt Review: Protects assets like your home and car from repossession as long as payments are maintained.

- Administration: Offers limited asset protection and may result in asset liquidation in some cases.

- Payment Distribution:

- Debt Review: Payments are managed through a Payment Distribution Agency (PDA), ensuring creditors receive their share.

- Administration: Payments are managed by an administrator and often result in higher fees.

- Impact on Credit Profile:

- Debt Review: Once completed and cleared, a clearance certificate restores your creditworthiness.

- Administration: Stays on your record for five years or until debts are fully paid.

Why Debt Review May Be Better

Debt review works well for individuals with significant debt who want to protect their assets and restructure payments. It also provides a clear path to becoming debt-free while avoiding creditor harassment.

Contact DCGsa for Expert Guidance – Registered Debt Counsellor with the National Credit Regulator NCRDC1560

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For more information about Debt Review – Click Here.

Debt Review or Administration? Understand the differences and choose the best solution for your financial needs with DCGsa’s expert guidance.

Debt counselling is a legal solution for individuals who are over-indebted and struggling to meet their financial obligations. To determine if you qualify, you need to meet specific criteria outlined in the National Credit Act.

Are you eligible for debt counselling? Let DCGsa help you find out with a free, obligation-free assessment tailored to your financial situation.

Criteria for Debt Counselling Qualification

- Over-Indebtedness:

- You must be declared over-indebted by a debt counsellor who has done a full financial assessment.

- Consistent Income:

- You need a reliable source of income to commit to a restructured repayment plan. This can include a weekly, biweekly or monthly salary, income such as rental income, retirement fund income (not SASSA) or other regular income. If you earn commission or run your own business, more details will be considered to get to your average income and this will be used in your assessment.

- Legal Credit Agreements:

- Your debts must fall under regulated credit agreements, such as personal loans, credit cards, store accounts, home loans or vehicle finance. We cannot normally include debt where legal action has already taken place.

Common Signs That You Qualify

- You’re using credit to pay for basic living expenses.

- You’ve received default notices from creditors.

- You’re overwhelmed by calls from debt collectors.

- Your monthly debt repayments leave you with little or no money to cover your household needs.

What Happens After You Qualify?

Once you qualify, a registered debt counsellor will guide you through the process, including negotiating with your creditors, restructuring your payments, and offering legal protection.

Take the First Step with DCGsa – Registered Debt Counsellor

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For a free, confidential assessment to see if you qualify, read – Understanding Debt Review Benefits

Debt counselling is a structured process designed to help individuals who are overwhelmed by debt regain financial stability. By working with a registered debt counsellor, your financial obligations can be consolidated into a single, affordable monthly repayment plan, ensuring legal protection and peace of mind.

Step-by-Step Process of Debt Counselling

- Assessment:

- Your debt counsellor will assess your income, expenses, and debt obligations to determine if you are over-indebted.

- Budget Planning:

- A realistic budget is created to prioritize essential expenses while setting aside funds for debt repayment.

- Negotiation with Creditors:

- Your debt counsellor negotiates with creditors to reduce interest rates, waive fees, and extend repayment terms.

- Legal Protection:

- Once under debt review, you are legally protected from creditors taking legal action against you.

- Implementation of the Repayment Plan:

- You make a single monthly payment to a Payment Distribution Agency (PDA), which then distributes the funds to your creditors.

- Debt Clearance:

- Upon completion of the repayment plan, you receive a clearance certificate, signaling your debt-free status.

Wondering how debt review works? Here’s a simple step-by-step guide to achieving financial freedom with DCGsa.

- Upon completion of the repayment plan, you receive a clearance certificate, signaling your debt-free status.

Why Choose Debt Counselling?

Debt counselling not only helps you avoid repossession of your assets but also provides you with the tools and support to achieve long-term financial freedom. It is a regulated process under the National Credit Act, ensuring fairness and transparency. Our Debt Counsellor is Registered with the National Credit Regulator since 2010.

Contact DCGsa Today!

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For more details, explore our website www.dcgsa.co.za

DCGsa helps you consolidate debt without taking another loan. Affordable assistance for financial peace. NCRDC 1560.

Debt counselling in South Africa is a legal and regulated process designed to help individuals who are over-indebted regain control of their finances. Introduced under the National Credit Act (NCA) of 2005, this process assists consumers by restructuring their debt repayments into affordable installments, while offering legal protection from creditors.

Debt counselling offers a path to financial freedom, helping you manage your obligations while reducing stress. Discover how it can safeguard your future

Key Aspects of Debt Counselling / Debt Review

- Assessment: A registered debt counsellor evaluates your financial situation to determine if you are over-indebted.

- Negotiation: Your debt counsellor negotiates with creditors to reduce interest rates and extend repayment terms, consolidating debts into one manageable monthly payment.

- Legal Protection: While under debt review, you are protected from legal action by creditors as long as you comply with the restructured payment plan.

- Debt Clearance: Once your debts are fully paid, you will receive a clearance certificate, allowing you to rebuild your credit profile.

- Simplified Payments: Combine all your debts into a single, reduced monthly payment.

- Asset Protection: Safeguard your home, vehicle, and other assets from repossession.

- Financial Relief: Reduce stress by eliminating creditor harassment and late payment fees.

Why Choose DCGsa?

At DCGsa, we specialize in guiding South Africans through the debt counselling process with compassion and expertise. As a trusted NCR-registered debt counsellor, our goal is to help you regain financial independence and peace of mind.

How to Get Started

📞 Call us: 086 100 1047

📧 Email us: help@dcgsa.co.za

💬 WhatsApp us: 061 432 8499

▶️ Watch our videos on YouTube: DCGsa Debt Counselling Group

For a detailed overview of our debt counselling services, visit our About Us page.

Take Control of Your Financial Future Today!

Debt doesn’t have to define your life. Reach out to DCGsa now for a free and confidential debt assessment. Let us help you build a secure financial future.

✨ DCGsa is here to guide you every step of the way! ✨

")

{kind=link}